Code

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

plt.rcParams['figure.figsize'] = (10, 5)

# plt.style.use('fivethirtyeight')

plt.rcParams['image.cmap'] = 'inferno'Once you’ve got a model for predicting time series data, you need to decide if it’s a good or a bad model. This chapter coves the basics of generating predictions with models in order to validate them against “test” data.

This Validating and Inspecting Time Series Models is part of Datacamp course: Machine Learning for Time Series Data in Python

This is my learning experience of data science through DataCamp

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

plt.rcParams['figure.figsize'] = (10, 5)

# plt.style.use('fivethirtyeight')

plt.rcParams['image.cmap'] = 'inferno'In machine learning for time series, it’s common to use information about previous time points to predict a subsequent time point.

In this exercise, you’ll “shift” your raw data and visualize the results. You’ll use the percent change time series that you calculated in the previous chapter, this time with a very short window. A short window is important because, in a real-world scenario, you want to predict the day-to-day fluctuations of a time series, not its change over a longer window of time.

prices = pd.read_csv('dataset/prices_nyse.csv', index_col=0, parse_dates=True)

prices = prices[['AAPL']]

# Your custom function

def percent_change(series):

# Collect all *but* the last value of this window, then the final value

previous_values = series[:-1]

last_value = series[-1]

# Calculate the % difference between the last value and the mean of earlier values

percent_change = (last_value - np.mean(previous_values)) / np.mean(previous_values)

return percent_change

def replace_outliers(series):

# Calculate the absolute difference of each timepoint from the series mean

absolute_differences_from_mean = np.abs(series - np.mean(series))

# Calculate a mask for the difference that are > 3 standard deviations from zero

this_mask = absolute_differences_from_mean > (np.std(series) * 3)

# Replace these values with the median across the data

series[this_mask] = np.nanmedian(series)

return series

# Apply your custom function and plot

prices_perc = prices.rolling(20).apply(percent_change)

# Apply your preprocessing functino to the timeseries and plot the results

prices_perc = prices_perc.apply(replace_outliers)# These are the "time lags"

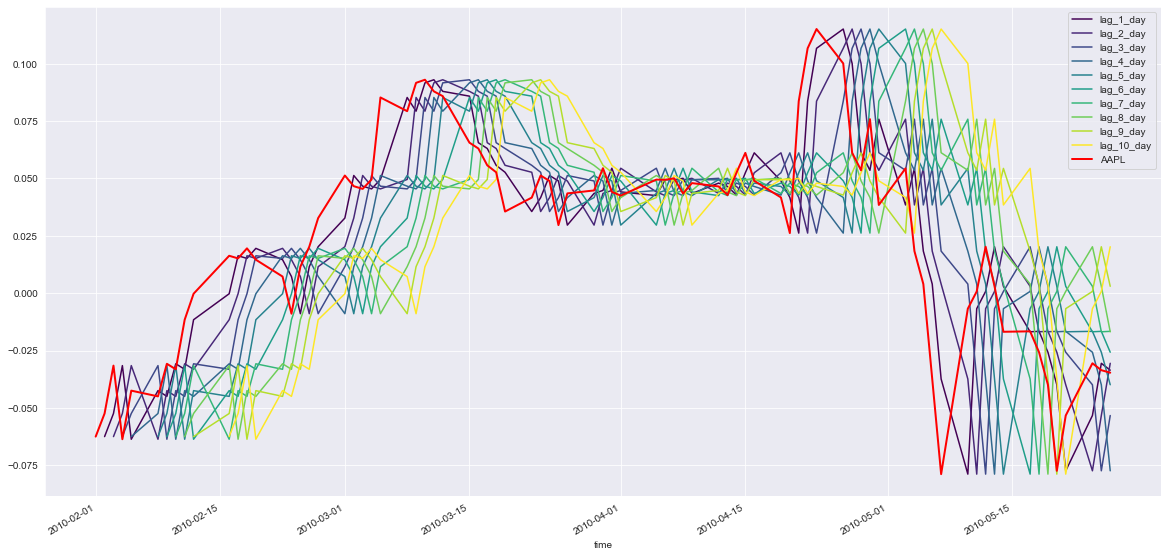

shifts = np.arange(1, 11).astype(int)

# Use a dictionary comprehension to create name: value pairs, one pair per shift

shifted_data = {"lag_{}_day".format(day_shift):

prices_perc['AAPL'].shift(day_shift) for day_shift in shifts}

# Convert into a DataFrame for subsequent use

prices_perc_shifted = pd.DataFrame(shifted_data)

# Plot the first 100 samples of each

fig, ax = plt.subplots(figsize=(20, 10));

prices_perc_shifted.iloc[:100].plot(cmap=plt.cm.viridis, ax=ax);

prices_perc.iloc[:100].plot(color='r', lw=2, ax=ax);

ax.legend(loc='best');

Now that you’ve created time-shifted versions of a single time series, you can fit an auto-regressive model. This is a regression model where the input features are time-shifted versions of the output time series data. You are using previous values of a timeseries to predict current values of the same timeseries (thus, it is auto-regressive).

By investigating the coefficients of this model, you can explore any repetitive patterns that exist in a timeseries, and get an idea for how far in the past a data point is predictive of the future.

from sklearn.linear_model import Ridge

# Replace missing values with the median for each column

X = prices_perc_shifted.fillna(np.nanmedian(prices_perc_shifted))

y = prices_perc['AAPL'].fillna(np.nanmedian(prices_perc['AAPL']))

# Fit the model

model = Ridge()

model.fit(X, y)Ridge()In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

Ridge()

Now that you’ve fit the model, let’s visualize its coefficients. This is an important part of machine learning because it gives you an idea for how the different features of a model affect the outcome.

In this exercise, you will create a function that, given a set of coefficients and feature names, visualizes the coefficient values.

def visualize_coefficients(coefs, names, ax):

# Make a bar plot for the coefficients, including their names on the x-axis

ax.bar(names, coefs);

ax.set(xlabel='Coefficient name', ylabel='Coefficient value');

# set formatting so it looks nice

plt.setp(ax.get_xticklabels(), rotation=45, horizontalalignment='right');

plt.tight_layout();

return ax# Visualize the output data up to "2011-01"

fig, axs = plt.subplots(2, 1, figsize=(10, 5))

y.loc[:'2011-01'].plot(ax=axs[0], ylim=(-0.1, 0.2));

# Run the function to visualize model's coefficients

visualize_coefficients(model.coef_, prices_perc_shifted.columns, ax=axs[1]);

Now, let’s re-run the same procedure using a smoother signal. You’ll use the same percent change algorithm as before, but this time use a much larger window (40 instead of 20). As the window grows, the difference between neighboring timepoints gets smaller, resulting in a smoother signal. What do you think this will do to the auto-regressive model?

# Apply your custom function and plot

prices_perc = prices.rolling(40).apply(percent_change)

# Apply your preprocessing functino to the timeseries and plot the results

prices_perc = prices_perc.apply(replace_outliers)

# Use a dictionary comprehension to create name: value pairs, one pair per shift

shifted_data = {"lag_{}_day".format(day_shift):

prices_perc['AAPL'].shift(day_shift) for day_shift in shifts}

# Convert into a DataFrame for subsequent use

prices_perc_shifted = pd.DataFrame(shifted_data)

# Replace missing values with the median for each column

X = prices_perc_shifted.fillna(np.nanmedian(prices_perc_shifted))

y = prices_perc['AAPL'].fillna(np.nanmedian(prices_perc['AAPL']))

# Fit the model

model = Ridge()

model.fit(X, y)Ridge()In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

Ridge()

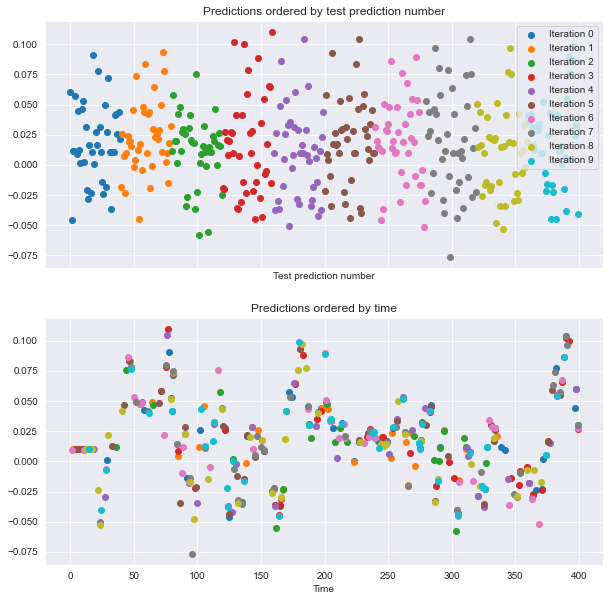

As you’ll recall, cross-validation is the process of splitting your data into training and test sets multiple times. Each time you do this, you choose a different training and test set. In this exercise, you’ll perform a traditional ShuffleSplit cross-validation on the company value data from earlier. Later we’ll cover what changes need to be made for time series data. The data we’ll use is the same historical price data for several large companies.

X = pd.read_csv('dataset/x.csv', index_col=0).to_numpy()

y = pd.read_csv('dataset/y.csv', index_col=0).to_numpy()from sklearn.linear_model import LinearRegression

from sklearn.metrics import r2_score

model = LinearRegression()def visualize_predictions(results):

fig, axs = plt.subplots(2, 1, figsize=(10, 10), sharex=True)

# Loop through our model results to visualize them

for ii, (prediction, score, indices) in enumerate(results):

# Plot the predictions of the model in the order they were generated

offset = len(prediction) * ii

axs[0].scatter(np.arange(len(prediction)) + offset, prediction,

label='Iteration {}'.format(ii))

# Plot the predictions of the model according to how time was ordered

axs[1].scatter(indices, prediction)

axs[0].legend(loc="best")

axs[0].set(xlabel="Test prediction number", title="Predictions ordered by test prediction number")

axs[1].set(xlabel="Time", title="Predictions ordered by time")from sklearn.model_selection import ShuffleSplit

cv = ShuffleSplit(n_splits=10, random_state=1)

# Iterate through CV splits

results = []

for tr, tt in cv.split(X, y):

# Fit the model on training data

model.fit(X[tr], y[tr])

# Generate predictions on the test data, score the predictions, and collect

prediction = model.predict(X[tt])

score = r2_score(y[tt], prediction)

results.append((prediction, score, tt))

# Custom function to quickly visualize predictions

visualize_predictions(results)

If you look at the plot to the right, see that the order of datapoints in the test set is scrambled. Let’s see how it looks when we shuffle the data in blocks.

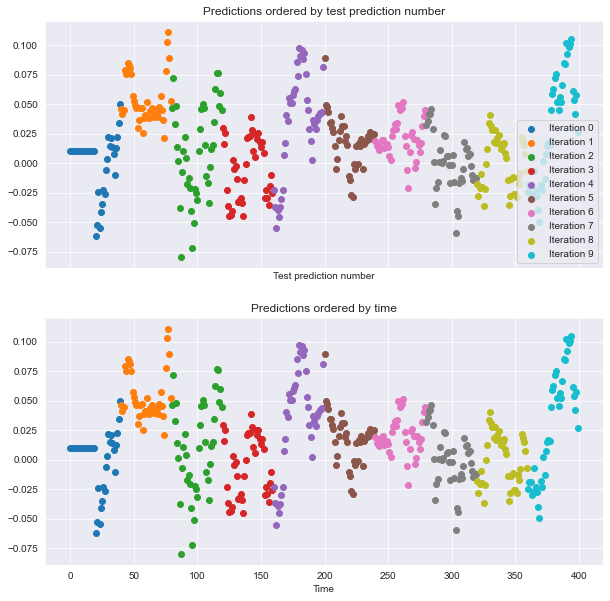

Now, re-run your model fit using block cross-validation (without shuffling all datapoints). In this case, neighboring time-points will be kept close to one another. How do you think the model predictions will look in each cross-validation loop?

# Create KFold cross-validation object

from sklearn.model_selection import KFold

cv = KFold(n_splits=10, shuffle=False)

# Iterate through CV splits

results = []

for tr, tt in cv.split(X, y):

# Fit the model on training data

model.fit(X[tr], y[tr])

# Generate predictions on the test data and collect

prediction = model.predict(X[tt])

results.append((prediction, _, tt))

# Custom function to quickly visualize predictions

visualize_predictions(results)

This time, the predictions generated within each CV loop look ‘smoother’ than they were before - they look more like a real time series because you didn’t shuffle the data. This is a good sanity check to make sure your CV splits are correct

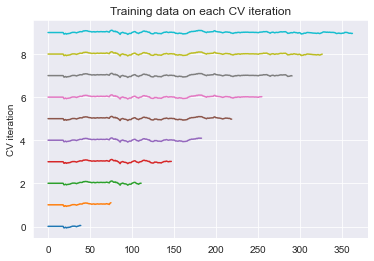

Finally, let’s visualize the behavior of the time series cross-validation iterator in scikit-learn. Use this object to iterate through your data one last time, visualizing the training data used to fit the model on each iteration.

from sklearn.model_selection import TimeSeriesSplit

# Create time-series cross-validation object

cv = TimeSeriesSplit(n_splits=10)

# Iterate through CV splits

fig, ax = plt.subplots()

for ii, (tr, tt) in enumerate(cv.split(X, y)):

# Plot the training data on each iteration, to see the behavior of the CV

ax.plot(tr, ii + y[tr]);

ax.set(title='Training data on each CV iteration', ylabel='CV iteration');

Note that the size of the training set grew each time when you used the time series cross-validation object. This way, the time points you predict are always after the timepoints we train on.

TimeSeriesSplit, can plot the model’s score over timeA useful tool for assessing the variability of some data is the bootstrap. In this exercise, you’ll write your own bootstrapping function that can be used to return a bootstrapped confidence interval.

This function takes three parameters: a 2-D array of numbers (data), a list of percentiles to calculate (percentiles), and the number of boostrap iterations to use (n_boots). It uses the resample function to generate a bootstrap sample, and then repeats this many times to calculate the confidence interval.

from sklearn.utils import resample

def bootstrap_interval(data, percentiles=(2.5, 97.5), n_boots=100):

"""Bootstrap a confidence interval for the mean of columns of a 1- or 2-D dataset."""

# Create our empty array we'll fill with the results

if data.ndim == 1:

data = data[:, np.newaxis]

data = np.atleast_2d(data)

bootstrap_means = np.zeros([n_boots, data.shape[-1]])

for ii in range(n_boots):

# Generate random indices for our data *with* replacement, then take the sample mean

random_sample = resample(data)

bootstrap_means[ii] = random_sample.mean(axis=0)

# Compute the percentiles of choice for the bootstrapped means

percentiles = np.percentile(bootstrap_means, percentiles, axis=0)

return percentilesIn this lesson, you’ll re-run the cross-validation routine used before, but this time paying attention to the model’s stability over time. You’ll investigate the coefficients of the model, as well as the uncertainty in its predictions.

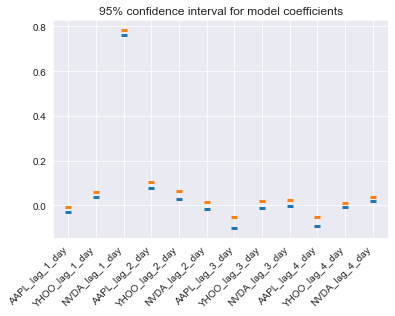

Begin by assessing the stability (or uncertainty) of a model’s coefficients across multiple CV splits. Remember, the coefficients are a reflection of the pattern that your model has found in the data.

X = pd.read_csv('dataset/stock_12x.csv', index_col=0).to_numpy()

y = pd.read_csv('dataset/stock_12y.csv', index_col=0).to_numpy()

feature_names = np.array(['AAPL_lag_1_day', 'YHOO_lag_1_day', 'NVDA_lag_1_day', 'AAPL_lag_2_day',

'YHOO_lag_2_day', 'NVDA_lag_2_day', 'AAPL_lag_3_day', 'YHOO_lag_3_day',

'NVDA_lag_3_day', 'AAPL_lag_4_day', 'YHOO_lag_4_day', 'NVDA_lag_4_day'])

times_scores = pd.DatetimeIndex(['2010-04-05', '2010-04-28', '2010-05-21', '2010-06-16',

'2010-07-12', '2010-08-04', '2010-08-27', '2010-09-22',

'2010-10-15', '2010-11-09', '2010-12-03', '2010-12-29',

'2011-01-24', '2011-02-16', '2011-03-14', '2011-04-06',

'2011-05-02', '2011-05-25', '2011-06-20', '2011-07-14',

'2011-08-08', '2011-08-31', '2011-09-26', '2011-10-19',

'2011-11-11', '2011-12-07', '2012-01-03', '2012-01-27',

'2012-02-22', '2012-03-16', '2012-04-11', '2012-05-04',

'2012-05-30', '2012-06-22', '2012-07-18', '2012-08-10',

'2012-09-05', '2012-09-28', '2012-10-23', '2012-11-19',

'2012-12-13', '2013-01-09', '2013-02-04', '2013-02-28',

'2013-03-25', '2013-04-18', '2013-05-13', '2013-06-06',

'2013-07-01', '2013-07-25', '2013-08-19', '2013-09-12',

'2013-10-07', '2013-10-30', '2013-11-22', '2013-12-18',

'2014-01-14', '2014-02-07', '2014-03-05', '2014-03-28',

'2014-04-23', '2014-05-16', '2014-06-11', '2014-07-07',

'2014-07-30', '2014-08-22', '2014-09-17', '2014-10-10',

'2014-11-04', '2014-11-28', '2014-12-23', '2015-01-20',

'2015-02-12', '2015-03-10', '2015-04-02', '2015-04-28',

'2015-05-21', '2015-06-16', '2015-07-10', '2015-08-04',

'2015-08-27', '2015-09-22', '2015-10-15', '2015-11-09',

'2015-12-03', '2015-12-29', '2016-01-25', '2016-02-18',

'2016-03-14', '2016-04-07', '2016-05-02', '2016-05-25',

'2016-06-20', '2016-07-14', '2016-08-08', '2016-08-31',

'2016-09-26', '2016-10-19', '2016-11-11', '2016-12-07'], name='date')

model = LinearRegression()# Iterate through CV splits

n_splits = 100

cv = TimeSeriesSplit(n_splits)

# Create empty array to collect coefficients

coefficients = np.zeros([n_splits, X.shape[1]])

for ii, (tr, tt) in enumerate(cv.split(X, y)):

# Fit the model on training data and collect the coefficients

model.fit(X[tr], y[tr])

coefficients[ii] = model.coef_# Calculate a confidence interval around each coefficient

bootstrapped_interval = bootstrap_interval(coefficients)

# Plot it

fig, ax = plt.subplots()

ax.scatter(feature_names, bootstrapped_interval[0], marker='_', lw=3);

ax.scatter(feature_names, bootstrapped_interval[1], marker='_', lw=3);

ax.set(title='95% confidence interval for model coefficients');

plt.setp(ax.get_xticklabels(), rotation=45, horizontalalignment='right');

Now that you’ve assessed the variability of each coefficient, let’s do the same for the performance (scores) of the model. Recall that the TimeSeriesSplit object will use successively-later indices for each test set. This means that you can treat the scores of your validation as a time series. You can visualize this over time in order to see how the model’s performance changes over time.

def my_pearsonr(est, X, y):

# Generate predictions and convert to a vector

y_pred = est.predict(X).squeeze()

# Use the numpy "corrcoef" function to calculate a correlation matrix

my_corrcoef_matrix = np.corrcoef(y_pred, y.squeeze())

# Return a single correlation value from the matrix

my_corrcoef = my_corrcoef_matrix[1, 0]

return my_corrcoeffrom sklearn.model_selection import cross_val_score

from functools import partial

# Generate scores for each split to see how the model performs over time

scores = cross_val_score(model, X, y, cv=cv, scoring=my_pearsonr)

# Convert to a Pandas Series object

scores_series = pd.Series(scores, index=times_scores, name='score')

# Bootstrap a rolling confidence interval for the mean score

scores_lo = scores_series.rolling(20).aggregate(partial(bootstrap_interval, percentiles=2.5))

scores_hi = scores_series.rolling(20).aggregate(partial(bootstrap_interval, percentiles=97.5))C:\Users\dghr201\AppData\Local\Temp\ipykernel_39244\1687367918.py:7: FutureWarning: Support for multi-dimensional indexing (e.g. `obj[:, None]`) is deprecated and will be removed in a future version. Convert to a numpy array before indexing instead.

data = data[:, np.newaxis]# Plot the results

fig, ax = plt.subplots()

scores_lo.plot(ax=ax, label='Lower confidence interval');

scores_series.plot(ax=ax, label='scores')

scores_series.rolling(20).mean().plot(ax=ax, label='rolling mean')

scores_hi.plot(ax=ax, label='Upper confidence interval');

ax.legend();

In this exercise, you will again visualize the variations in model scores, but now for data that changes its statistics over time.

# Pre-initialize window sizes

window_sizes = [25, 50, 75, 100]

# Create an empty DataFrame to collect the stores

all_scores = pd.DataFrame(index=times_scores)

# Generate scores for each split to see how the model performs over time

for window in window_sizes:

# Create cross-validation object using a limited lookback window

cv = TimeSeriesSplit(n_splits=100, max_train_size=window)

# Calculate scores across all CV splits and collect them in a DataFrame

this_scores = cross_val_score(model, X, y, cv=cv, scoring=my_pearsonr)

all_scores['Length {}'.format(window)] = this_scores# Visualize the scores

ax = all_scores.rolling(10).mean().plot(cmap=plt.cm.coolwarm);

ax.set(title='Scores for multiple windows', ylabel='Correlation (r)');

tsfresh)